Should I invest in Crypto?

What lessons can we learn from the collapse of FTX?

The swift and total collapse of the cryptocurrency online exchange FTX has created a shockwave throughout the crypto industry. Once a company valued at $32 billion, FTX collapsed seemingly overnight, filing for Chapter 11 bankruptcy. The company, facing a liquidity crunch from investors withdrawing billions a day, sought help from rival crypto exchange Binance. On November 8th, Binance signed a nonbinding agreement to rescue FTX, essentially bailing them out of their liquidity woes. But after only a two-hour examination of the company’s balance sheet, Binance deemed them “beyond saving” and backed out of the deal. The crypto exchange giant collapsed in just a matter of days, and crypto investors have lost $1-2 billion. FTX founder Sam Bankman-Fried has since stepped down as CEO and admitted, “I f**ked up. Big. Multiple times.” Newly appointed CEO John Ray III said, “In his 40 years of legal and restructuring experience,” he had never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.” When the CEO who oversaw Enron’s bankruptcy concludes that…you know you messed up.

Now I could talk about all the shady and illegal misuse of funds between FTX and its affiliated companies like Sam’s hedge fund Alameda Research or the propping up of its cryptocurrency FTT. I could give a robust biography detailing Sam’s meteoric rise and catastrophic fall reminiscent of other fraudsters. Elizabeth Holmes, Bernie Madoff, and Billy McFarland come to mind. Or we could look at his $40 million in donations and political ties to the Democratic Party. I could talk about the company mismanagement, lack of financial safeguards, or the company’s risky acquisitions like that of the Miami Heat Arena. I could go on and on. That’s not the purpose of this article. The purpose of this article is to inform you of the risks associated with investing in crypto before making any investment decisions. What lessons can we derive from the collapse of FTX?

What is crypto?

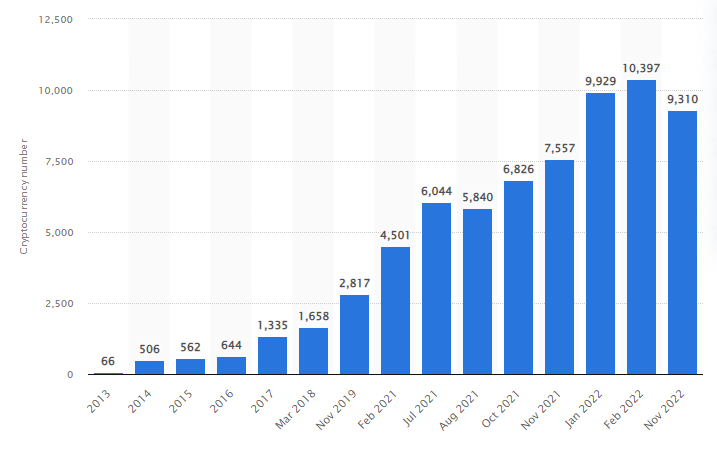

Crypto is a decentralized digital currency using blockchain technology. Without going into the complexities of how blockchain works, it’s essentially a digital database or ledger consisting of a network of computers that authenticate and record transactions without the use of a third-party like a bank or a government. In this way, crypto is said to be ‘decentralized’ because no central institution or authority is controlling or overseeing the transactions. According to data from Statistica, there are over 9,000 cryptocurrencies in existence today with new ones popping up all the time. The bar graph below shows the dramatic rise in cryptocurrencies since 2013. For the sake of this article, we will only examine the largest and most popular cryptocurrency, Bitcoin.

Crypto is a relatively new asset class.

Cryptocurrency hasn’t been around for that long. The first cryptocurrency came on the scene with the launch of Bitcoin in January 2009. Today, the market cap of Bitcoin has reached over $300 billion. Given that Bitcoin is so new, that means we only have 13 years of price data to analyze. By contrast, trading in commodities like gold has been around for hundreds of years. The US stock market has existed for over 200 years. Even exchange-traded funds (ETFs) have been trading more than a quarter of a century. The issue with crypto as opposed to more traditional assets like stocks or bonds is that it’s more difficult to predict the long-term trend because of the limited data. Take stocks for example. Here’s an inflation-adjusted, historical chart of the S&P 500 index over the last 95 years from 1927 to today. If you look at the long-term trajectory, the S&P 500 goes up on average 7-10% per year. Yes, you see those short-term dips that we call corrections or bear markets, but the long-term trend is upward. We don’t have that kind of long-term data with Bitcoin, because it’s such a new asset.

Crypto ix extremely volatile.

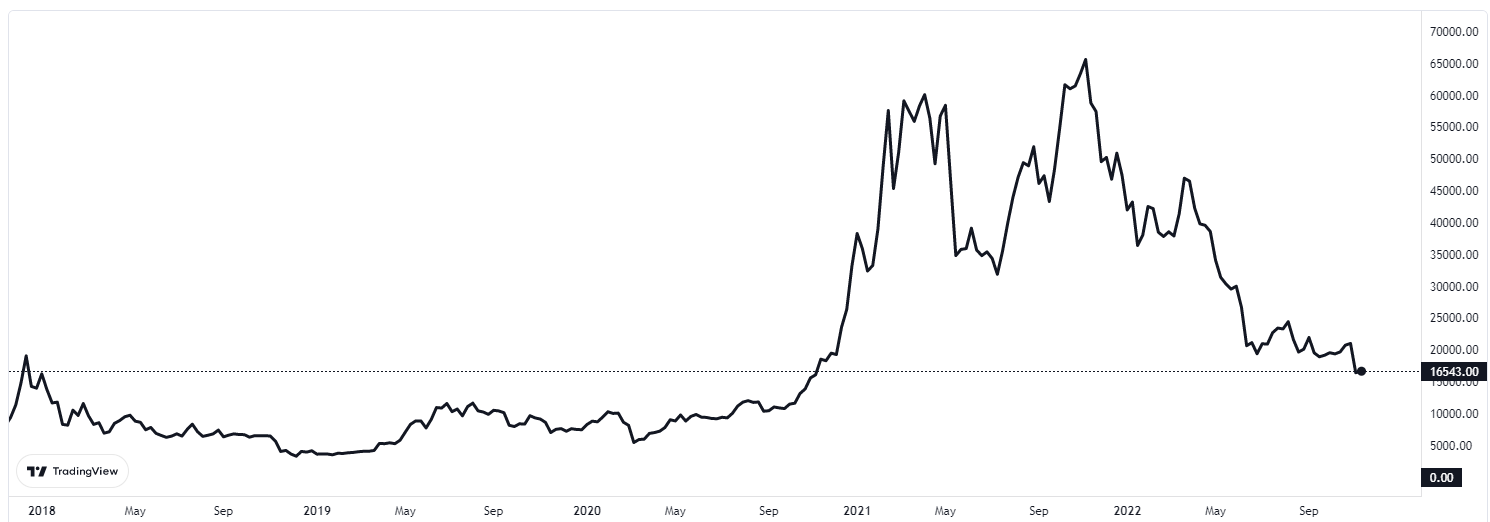

Crypto is an extremely volatile asset class. Just look at the chart below, which depicts the price of Bitcoin over the last five years. There’s no discernible long-term trend whatsoever. It’s all about luck and timing. If you invested $1,000 in March of 2020 at a Bitcoin low-point, you would have approximately $11,913 as of November 19th. That is an astounding 1,191% gain in only 20 months! On the other hand, if you got in at Bitcoin’s peak in November of 2021 with $1,000, you would have only $240 today. That’s a 76% decrease in value! Huge price swings are common for Bitcoin and especially other, smaller cryptocurrencies on a week-to-week sometimes even day-to-day basis.

Crypto is fairly unregulated.

Another issue with crypto is that it’s not well-regulated. Like I mentioned earlier, crypto has only been around since 2009. Because it’s such a new asset, government regulations are having to play catch-up. There is still an ongoing debate on how to classify crypto let alone regulate it. The catastrophe of FTX has only hastened the call for more regulation. Congressman Patrick McHenry (R-NC) and Congresswoman Maxine Waters (D-CA) have announced a bipartisan House Financial Services Committee investigation into the “collapse of FTX and its broader consequences for the digital asset ecosystem.” These events will undoubtedly lead to more rules and restrictions in the crypto space. All this upcoming legislation will add even more uncertainty to the crypto market and its role in our financial ecosystem.

Crypto is fraught with fraud, bankruptcies, and scams.

Instances of illicit or unethical activity have become more and more prevalent in the crypto space. As of July, hackers have stolen nearly $2 billion worth of crypto this year. Decentralized finance platforms are more vulnerable to cybercriminals. These hackers can study the open-source code, exploit its weaknesses, and steal crypto funds. With the emergency of new cryptocurrencies, scams have increased too. Since the start of 2021, more than 46,000 people have reported losing over $1 billion in crypto to scams. Even the so-called ‘stablecoins’ are not stable. Look at the case of stablecoin TerraUSD (UST) and its nonstable, counterpart coin LUNA from the crypto project Terra. These coins were touted to be a relatively safe haven in the volatile crypto market. Using computer algorithms and game theory, the stablecoin TerraUSD (UST) was supposed to be tied to the value of the US dollar at a 1-to-1 peg ratio. UST was supposed to then act as a support for the value of its sister token LUNA, which could fluctuate in value. You could exchange one coin for another and vice versa. After a rapid series of withdrawals, UST lost its peg to the US dollar. Once valued at almost $160, LUNA collapsed in May, losing 99% of its value in only a few days.

These examples remind us once again that crypto has no government or central bank underpinning. If you have money at a bank, and the bank goes under, you’re covered by FDIC protection. If you have securities at a brokerage firm, and they file for bankruptcy, you have SIPC insurance. Or if fraud occurs and your money is stolen, these institutions will reimburse you. Because of its decentralized nature, there are no similar legal protections for crypto assets.

There is a key lesson to be learned from the collapse of FTX—there is no such thing as a free lunch. The crypto space is in its infancy, and it’s fairly unregulated. You could lose millions in a matter of days. Your hard-earned cash could be stolen right from under your nose, or your life savings could be wiped out right in front of your eyes. Investors see an asset like bitcoin skyrocket in such a short time and experience FOMO or ‘Fear-Of-Missing-Out.’ They don’t want to miss out on winning the ‘jackpot.’ They go ‘all-in’ without due diligence or research, and they are soon left high and dry. If it’s too good to be true, it probably is. Now, I don’t mean to bad-mouth Bitcoin or disparage the crypto market as a whole. The point that I am trying to make here is this: don’t invest in something that you don’t understand. Take the time to research beforehand. If you have done your homework and you know the risks, go for it. Just make sure you read the fine print before you do.