Over the past few months, we have seen financial markets take a tumble. The S&P 500 index has dipped 23.7% from its previous all-time high in early January. This index tracks the stocks of the 500 largest publicly traded companies in the US, making it a good overall measure of the total US stock market. This recent dip marks our descent into bear market territory (when the S&P index goes down 20% from a previous high). If you watch the news, it may feel like the sky is falling. Inflation is at a 40-year high, supply chain issues continue to disrupt the market, Russia’s invasion of Ukraine drags on, and the US economy teeters on the brink of a potential recession. I have worked in the finance industry almost three years now. I spoke with hundreds of clients throughout the Covid pandemic and the market crash. I know what you might be thinking. Your accounts are in the red; you see them drop daily. All this uncertainty and volatility makes you anxious, which leads to fear, which leads to panic. You can’t stomach these losses anymore. You can’t sleep at night. You’re thinking about selling and cutting your losses to stop the bleeding. Stop right there! Not another move! Before you make any rash decisions, hear me out. Here are some things to ponder before you sell.

Bear markets are completely normal.

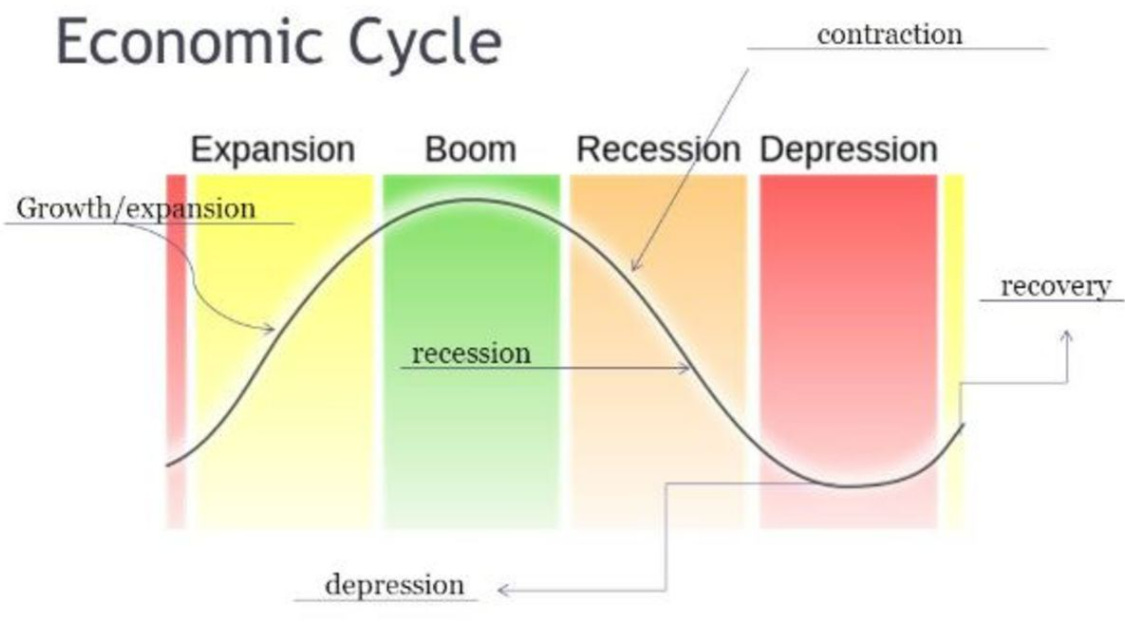

Financial markets occur in cycles, and bear markets are just another regular part of that cycle. Think of the market cycle similar to the four seasons. First, we have the early cycle or expansion phase (spring). The market begins to recover, company earnings accelerate, and GDP increases. Stocks tend to perform very well in this stage. Second, we have the mid-cycle phase or boom (summer), where earnings and GDP growth peak. Historically, this is another great season for stocks. After growth peaks, things start to slow down. Third, we see the late-cycle phase or recession (fall), where earnings growth begins to decelerate. Fourth, we have the depression phase (winter), where earnings contract and GDP decreases. Stocks tend to perform poorly in these conditions. We are currently in the recession phase of the market cycle. This is the phase that most people fear. They see the market tank, and their first instinct is to sell. However, as I have shown, everything happens in a cycle. The figure below illustrates this market cycle.

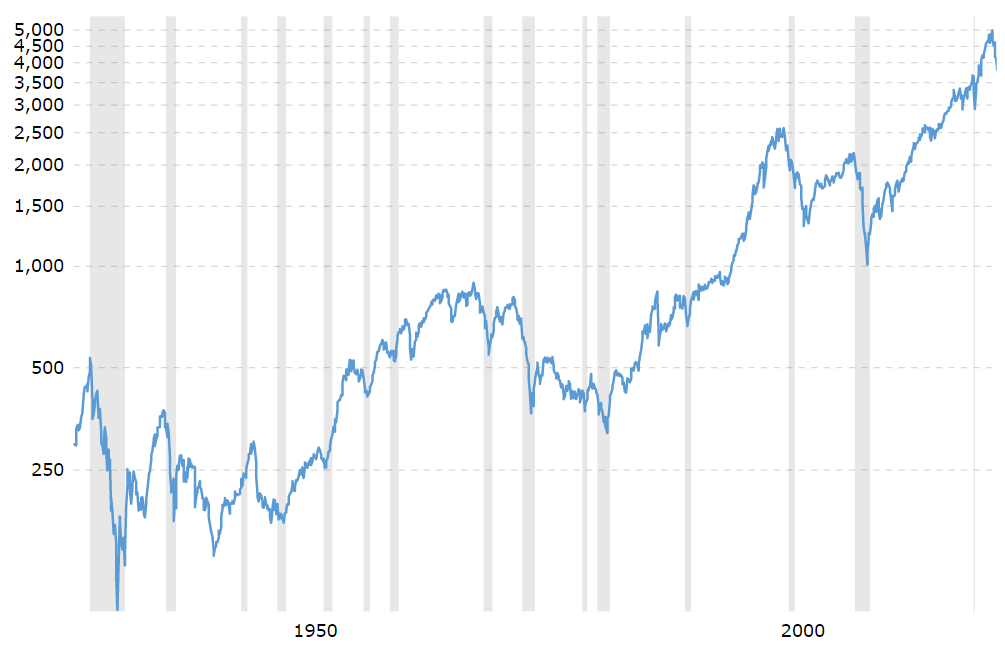

The market has never not reached a new all-time high.

Forgive my double negative, but it’s true! If you look at a chart of the S&P over many years, it continues to climb. Despite the short-term dips you see along the way, the long-term market trajectory is up. The short-term dips correspond to the corrections (10% decreases) and bear markets (20% decreases) that have occurred over the last 100 years, which, like I mentioned before, are completely normal. Excluding the current bear market and going back to the Stock Market Crash of 1929, there have been approx. 18 bear markets. The average bear market lasts 19 months and yields an average S&P drawback of 30% with a full recovery time of 48 months. In my last article, I explained the difference between recession bear markets and non-recession bear markets. A contraction of corporate earnings and a decrease in GDP lead to a recession bear market, while only a decline in stock valuation accompanies a non-recession bear market. Non-recession bear markets are much shorter. They tend to last only four months and produce an S&P drawback of 22% with a full recovery time of 11 months. The point that I am trying to make here is that, if history has anything to show us, the market always recovers. These recessions and bear markets don’t last forever.

Timing the market is extremely difficult.

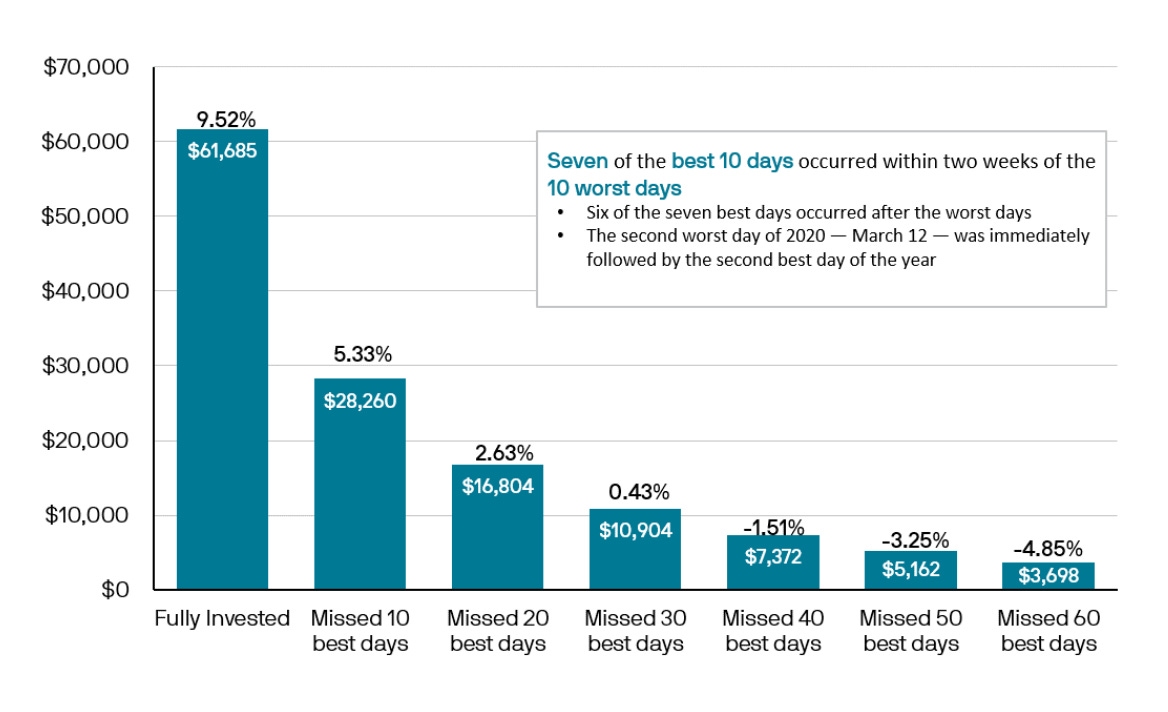

Jumping in and out of the market in an attempt to time market tops and bottoms can severely decrease your return. The best market days often follow the worst ones. In fact, seven of the 10 best market days occurred within two weeks of the 10 worst days, and six of the best seven days occurred after the worst days measured over a period of 20 years shown below. If you sell out, when will you get back in? What will you look for? Most investors won’t know when to get back in. They will wait for the market to recover and by then miss out on tangible market gains. The chart below illustrates this principle. What you see is the performance of a $10,000 investment tracked over 20 years from January 1st, 2002, to December 31st, 2021. If you missed out on the 10 best trading days, your final balance would be cut more than half at a whopping 54% decrease. There’s no perfect signal to get out of the market before a collapse, and market bottoms are only determined in hindsight.

Where are we headed?

The big question that I first brought up in my last article is whether or not the US will enter a recession. As I have showed above, the gap in recovery time and market pullback % between recession bear markets and their non-recession counterparts is not insignificant. When asked if the US is headed for a recession in the next 6-12 months, Jurrien Timmer, director of global macro in Fidelity’s Global Asset Allocation Division, responded, “I personally don't think so. I don't see a lot of evidence to suggest that we are. Consumers are employed. The jobless rate is very low. Consumers still have savings from the pandemic era, but inflation is eroding disposable income, so people have less money to spend. Therefore, they're choosing how to spend it, and we're seeing that consumers are spending less money on big-ticket items like TVs and furniture, and instead they're spending it on travel. So there's a change in how consumers are spending. But from what I'm seeing there's very little evidence to suggest that we are headed headlong into a recession.”

What should you do?

Your 1# priority when it comes to saving and investing is having an emergency fund. Regardless of who you are, everyone should have an emergency fund that covers 3-6 months of living expenses. Life is full of unexpected expenses and emergencies. You want the money to be there when you need it. Otherwise, you may have to lock in a loss and sell out of long-term investments to free up the funds. After you have an emergency fund, you can determine what your goal is for saving and investing. Are you saving for retirement, a new house, kids’ college fund, wealth accumulation, a new car? The goal of the account will determine how you should invest. Next, your time horizon (time you plan on investing) and your risk tolerance (how much risk you’re willing to take on) will influence how aggressive or conservative your investments should be.

The most important pillars of investing are asset allocation and diversification, which is how you spread your money across different asset classes. These are the biggest factors determining your risk level and returns. Unless you need the money in a short time frame, one of the worst things you can do is panic sell when the markets are down. You will lock in a loss, and you most likely won’t get back in when the market is farther down. The markets will eventually bounce back, and you’ll miss out on all those gains. When times get tough, it is essential that you don’t react emotionally and that you stick to your financial plan. If you don’t have the will, skill, or time to invest on your own, find a financial advisor to work with who will help you come up with that plan and stick to you it. If you need to adjust your asset allocation to something more conservative, by all means do it, but don’t make the impulsive decision to liquidate your entire portfolio based on fear of loss. You will end up losing more in the end.